Don't Let Home Insurers Fool You. They're More Profitable Than Ever

The industry paints a gloomy picture, but nationwide, property insurers still cleared $25.4 billion in underwriting profit in 2024, and their net investment income surged to $164.3 billion.

Soaring home insurance rates and coverage withdrawals are inseparable from the fossil fuel-driven climate crisis and the affordable housing crisis. The Revolving Door Project is trying to shed light on these problems in a way that contributes to equitable and sustainable solutions. To that end, it’s important to scrutinize assertions that the insurance industry is struggling. In fact, insurers are doing better than ever.

In 2022, Allstate halted the sale of new residential and commercial property insurance policies in California. The company cited growing wildfire risks, increased rebuilding costs, and rising reinsurance premiums. State Farm bailed the next year. Also in 2023, Farmers Group stopped accepting new applications for home insurance policies in Florida, citing hurricane exposure and mounting rebuilding costs. It’s not just the Golden State and the Sunshine State. Two years ago, AIG moved to curtail home insurance sales in about 200 ZIP codes around the country at heightened risk of wildfires or floods, affecting parts of more than a dozen states.

Since then, it’s become increasingly common to hear insurance giants point to escalating climate shocks as the reason they’re abandoning communities or jacking up rates. The industry narrative is that insurers are suffering devastating losses that threaten to put them out of business and therefore, the only sensible response is to retreat from especially vulnerable areas and hike premiums everywhere else.

But the industry’s well-worn story is highly misleading, for reasons that I explain below. It’s also insulting, given that insurance firms continue to profit from planet-wrecking fossil fuels through their underwriting and investments. If insurers stopped underwriting and investing in coal, oil, and gas—the primary sources of the greenhouse gas pollution causing more frequent and intense extreme weather—it would signal that they’re taking this crisis seriously; instead, in the absence of effective regulation, they’re socializing losses and maximizing profits while they can.

Concealing Investment Income and Moving the Goalposts

In spite of the insurance industry’s public pessimism campaign, business is booming, and executives are thriving. According to fresh data from the National Association of Insurance Commissioners (NAIC), property and casualty insurers made $166.8 billion in profit in 2024. These record-high profits, which include auto insurance, were up 91% from 2023 and 330% from 2022.

As the NAIC data (see table below) make clear, the property and casualty industry as a whole is doing well. The industry made $25.4 billion from underwriting last year, with premium revenue outpacing payouts and expenses. What’s more, the industry’s net investment income surged to $164.3 billion, up 36% from 2023, thanks to $84.9 billion in earned investment income plus realized capital gains of $79.5 billion.

Conveniently for insurers, their rising investment income is seldom mentioned amid discussions of their mounting climate-related losses. The suppression of this information is especially galling since the industry’s substantial fossil fuel investments contribute to worsening climate damages.

In addition to concealing their investment income, insurers routinely talk about underwriting profitability in a misleading way.

Looking at the NAIC data in the table above, “net loss ratio” refers to the sum of losses incurred plus loss adjustment expenses (i.e., the cost of investigating and settling claims) divided by premiums earned. Last year’s net loss ratio of 71.2% is lucrative because it means that for every dollar of premium revenue, insurers are forfeiting just 71 cents to pay out claims.

However, insurers typically exaggerate their “losses” by categorizing overhead (e.g., office space, advertising, and commissions) as underwriting expenses. Last year’s “expense ratio” (overhead divided by premiums written) was 25.2%. Insurers then put all of this together to come up with a so-called “combined ratio.” Of course, the combined ratio is much higher than the net loss ratio by itself, enabling insurers to erroneously claim poverty.

In 2023, for instance, the industry could point to $19.7 billion in “underwriting losses” (including overhead) or its combined ratio of 101.7% to claim that insurers were losing more money than they brought in, making them unprofitable. This only makes sense if you ignore the industry’s 2023 net investment income of $120.8 billion, which resulted in annual profits of $87.3 billion.

The Tampa Bay Times and Miami Herald recently revealed an especially egregious case of insurance industry dishonesty. According to the newspapers, several insurers in Florida reported losses to the state’s Office of Insurance Regulation while their executives funneled billions of dollars to affiliate companies. Executives used those obscured profits to shower shareholders with $680 million in dividends. In addition, they alluded to fabricated “losses” to persuade lawmakers to pass industry-friendly, anti-consumer legislation.

Fallacy of Composition

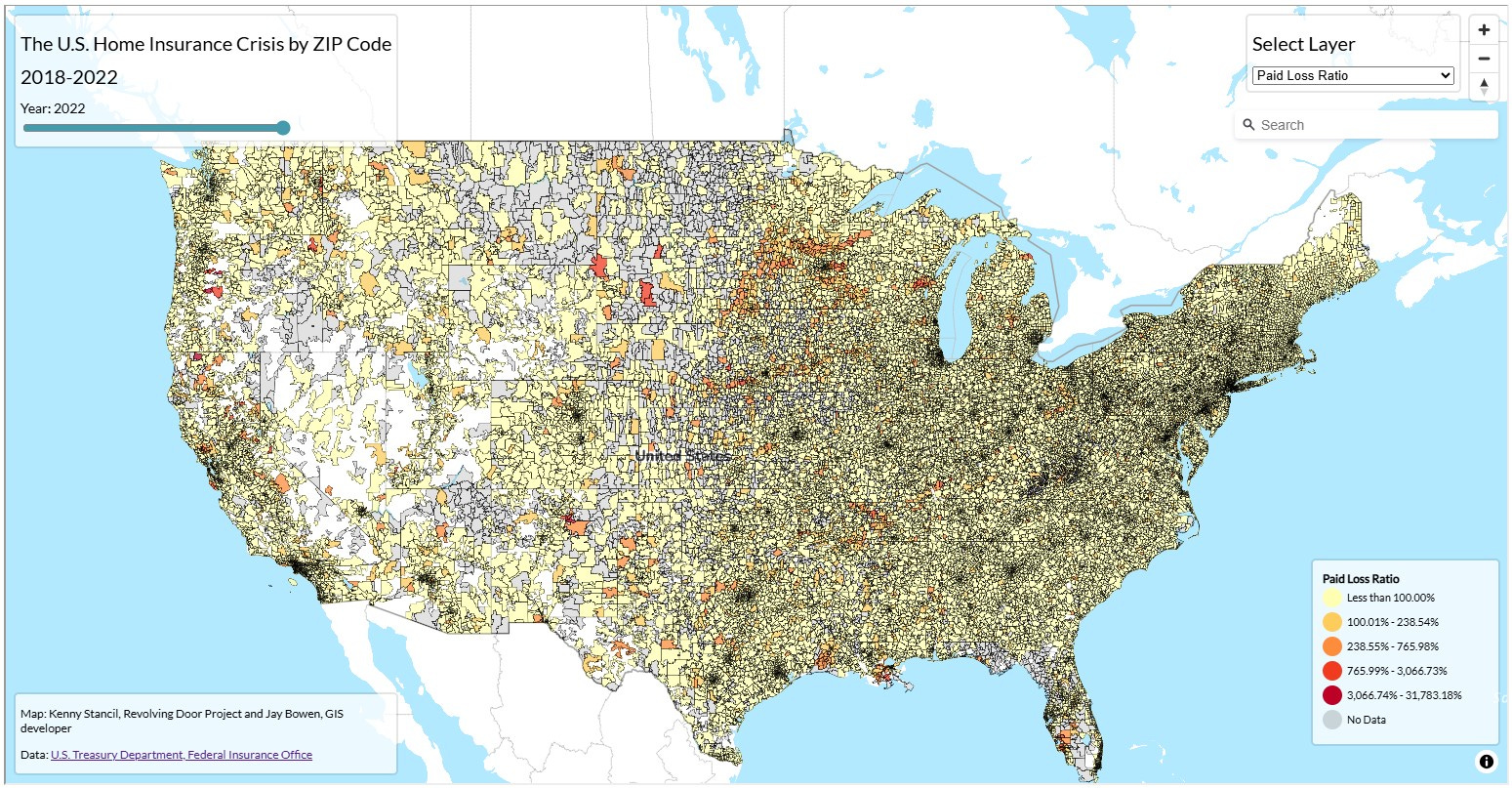

In its 2025 report on U.S. homeowners insurance markets, the Treasury Department’s Federal Insurance Office (FIO) used a simplified metric called a “paid loss ratio,” which it defined as “the amount insurers have paid on claims to or on behalf of policyholders relative to premiums received.”

A paid loss ratio of 100% signifies that an insurer’s claim payouts are equal to its premium revenue. A paid loss ratio above 100% is considered “negative” because it means that an insurer is paying out more than 100 cents for every dollar of premium revenue, while a paid loss ratio under 100% is considered “positive” for the opposite reason.

Suppose it were true that negative paid loss ratios (above 100%) signaled a lack of profitability. It’s not true because, as noted above, investment income is a major source of insurer profits. But for the sake of argument, let’s pretend it’s true.

Even if that were the case, insurer complaints about underwriting losses would still be wildly overblown.

I analyzed the dataset that FIO released in January. It encompasses 25,593 ZIP codes and covers the years 2018 to 2022. Here’s what I found:

In 2018, 23,346 of the 25,593 ZIP codes with data (91.2%) had positive paid loss ratios.

In 2019, 23,455 ZIP codes in the dataset (91.6%) had positive paid loss ratios.

In 2020, 23,217 of the ZIP codes (90.7%) had positive paid loss ratios.

In 2021, 23,456 of the ZIP codes (91.7%) had positive paid loss ratios.

In 2022: 23,114 of the ZIP codes (90.3%) had positive paid loss ratios.

So each year, premium revenue exceeded payouts in over 90% of ZIP codes, and the reverse was true in less than 10% of ZIP codes.

On top of the fact that the industry’s inclusion of overhead in its calculations muddies the waters, what we’re dealing with here is a fallacy of composition. The insurance industry is implying that what’s happening in some areas of the United States is indicative of what’s happening everywhere.

This fallacy can be seen in the map below, which comes from a recent report by the Revolving Door Project and Public Citizen. (Go here and select “Paid Loss Ratio” from the dropdown menu of the first interactive map.) Every year, insurers rake in more premium revenue than they pay out in claims in all but about 2,200 of the roughly 25,600 ZIP codes with data.

To suggest, as the insurance industry does, that underwriting losses incurred in less than 10% of the country constitute an existential financial threat is to miss the forest for the trees. In over 90% of the country, insurers are winning. Based on the NAIC data in the table above, which show that insurers’ national net loss ratio is typically around 70%, it’s safe to say that the volume of losses incurred in a minority of ZIP codes is not high enough to outweigh underwriting gains in the vast majority of ZIP codes. And yet, insurers are still nonrenewing policies and raising rates all over (check out “Nonrenewal Rate” and “Average Premiums” in the map’s dropdown menu).

One major issue is that reinsurance companies, which provide insurance for insurers, have been raising their prices in recent years. Insurance firms have been passing on the soaring cost of reinsurance to consumers. To reduce insurers’ reliance on the global reinsurance market, which is unregulated and highly concentrated, policymakers could develop a public reinsurance program.

Insurers Could Curb Climate Chaos If They Wanted To

The same insurance companies deserting and fleecing communities nationwide are using customers’ money to prop up fossil fuels, the leading cause of climate breakdown.

U.S. insurance firms, major players in the institutional investor sector, held between $536 billion and $582 billion in fossil fuel-related assets in 2019, the most recent year for which data is available.

In addition, insurers make billions from underwriting coal, oil, and gas projects. Eight U.S.-based companies alone collected $5.26 billion in premiums from fossil fuel clients in 2023, meaning the total is far higher.

Notably, premiums from fossil fuel underwriting represent a tiny fraction of total premiums. If they don’t already, insurers’ estimated climate losses will soon exceed their fossil fuel premiums anyway. This begs the question of why insurance firms continue to risk everything for such a relatively small revenue stream. The insurance industry’s own self-interest should compel it to ditch the dirty energy sector.

Ultimately, given that private insurers prioritize their own profits over social protection, it’s essential to remain skeptical of industry claims of victimhood and financial hardship.